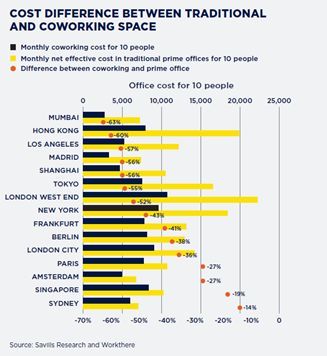

Research by Savills has revealed that renting a co-working office space for 10 people in Sydney or Singapore is only 14% and 19% cheaper respectively than occupying a traditional office. In comparison, coworking space is 63% cheaper than traditional offices in Mumbai, and 60% cheaper in Hong Kong.

In its Impacts global research programme, the international real estate advisor examined the cost of renting a co-working arrangement relative to the net effective cost of renting a conventional prime office for a 10-person business in 16 cities around the world. The study found that a co-working space is 40 per cent cheaper than a traditional space, on average, although there is considerable variation between locations. Sydney, Singapore, Amsterdam and Paris have the smallest gaps between the cost of coworking space versus traditional offices, while Mumbai, Hong Kong, Los Angeles and Madrid have the cheapest coworking space relative to what a tenant could expect to pay for a traditional office in these cities. On a purely cost basis, the lowest rents for co-working space can be found in Mumbai, Madrid, Shanghai, Amsterdam and Los Angeles, while New York and London are the most expensive, says Savills.

“Although co-working space can play many roles, it’s often viewed as an ‘affordable’ option for many SMEs and start-ups, enabling these businesses to invest in growth rather than rent”, says Cal Lee, global head of Workthere, Savills flexible office specialist. “For any mature office market wanting a strong base of start-up and scale-up businesses, it’s imperative there’s a diverse range of price points available but our analysis shows that in some locations the cost gap between a co-working space and a traditional office is narrow. This will be challenging to some businesses and probably push them out to lower cost areas on these cities’ peripheries. It’s important to get the balance right as these SMEs are often the lifeblood of the wider business ecosystem, and ultimately their absence will affect long-term growth.”

Jeremy Bates, head of occupational markets EMEA, Savills, adds: “We are seeing some examples of public-sector funds being used alongside private investment to provide subsidised space at lower prices, but we need more of this in key locations to maintain a supply of affordable options to ensure the longevity of cities’ business economies. Many ‘traditional’ office landlords have already incorporated some element of flex or serviced office space within their buildings, recognising its growing appeal to occupiers and the extra vibrancy it can bring to the business ecosystem, but this has potentially contributed to the narrowing rental gap between the two types as the boundaries have blurred.”

Jarosław Pilch, head of tenant representation, Savills Poland, and Head of Workthere.pl, comments: “In the Polish market, we also observe that building owners are increasingly accommodating the expectations of smaller tenants. We predict that in the upcoming years, having a flexible operator in modern office buildings will not only be desirable but necessary as well. This will allow for a restructuring of the leasing portfolio by consolidating smaller leases within a shared space, giving them time for development and freeing up space for larger organizations. Looking at the rental costs of flexible space in the center of Warsaw, it is comparable to entering into a 3-year traditional office lease agreement for an area of 300-400 square meters. This assumes that the tenant also had to make a financial contribution towards its arrangement, furnish conference rooms, provide office equipment and kitchen facilities, as well as hire someone to manage the reception.”

Jarosław Pilch, head of tenant representation, Savills Poland, and Head of Workthere.pl, comments: “In the Polish market, we also observe that building owners are increasingly accommodating the expectations of smaller tenants. We predict that in the upcoming years, having a flexible operator in modern office buildings will not only be desirable but necessary as well. This will allow for a restructuring of the leasing portfolio by consolidating smaller leases within a shared space, giving them time for development and freeing up space for larger organizations. Looking at the rental costs of flexible space in the center of Warsaw, it is comparable to entering into a 3-year traditional office lease agreement for an area of 300-400 square meters. This assumes that the tenant also had to make a financial contribution towards its arrangement, furnish conference rooms, provide office equipment and kitchen facilities, as well as hire someone to manage the reception.”