- Executive Note

- Editorial note

- Interviews

- Real Estate & Construction

- Events Coverage

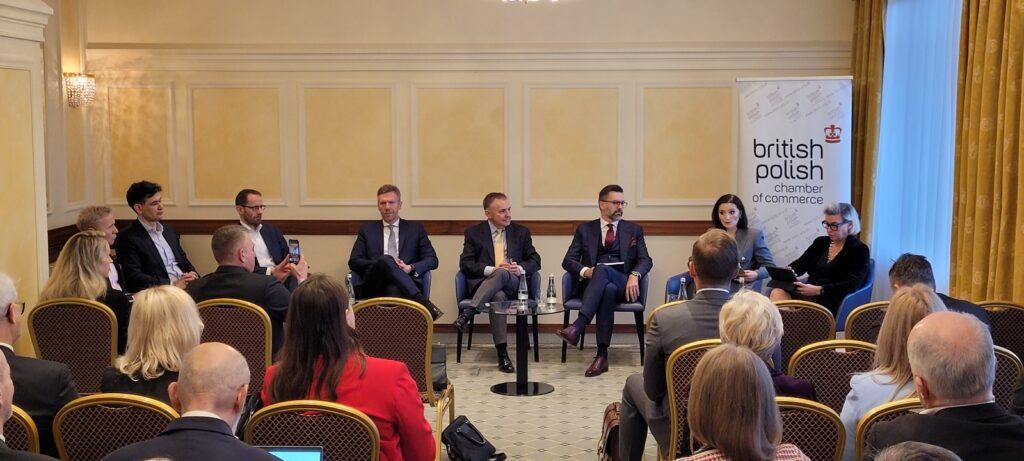

CEO Breakfast takes a hard look at 2023

British Polish Chamber of Commerce | Mar 9, 2023, 08:23

In the New Year, it’s a long-standing BPCC tradition to invite a panel of CEOs to discuss prospects for the year ahead for business in Poland. This year was no exception. After two years of being held online, this year’s expert panel took place live at Warsaw’s Polonia Palace Hotel on 11 January.

PwC’s chief economic advisor and several CEOs and senior managers representing different business sectors set out their views of how the Polish economy is expected to fare this year. They looked at 2023 in terms of new investments, growth, inflation and interest rates, consumer demand, green transformation, Russia’s invasion of Ukraine, European funding and how foreign perceptions might sway investment decisions in a general-election year.

After an introduction and welcome by Paweł Siwecki, the BPCC’s CEO, Prof Witold Orłowski, chief economic advisor, PwC Polska, set the scene at the macro level, after which Adam Uszpolewicz, former Aviva Poland CEO and BPCC board advisor, introduced the panel which consisted of Aneta Jóźwicka, corporate relations director Northern Europe, Diageo and BPCC chairwoman; Beata Balas-Noszczyk, managing partner, Hogan Lovells Poland; Paweł Bajorek, CEO for the CEE region, Reckitt; Tomasz Buras, CEO, Savills Poland; Piotr Kuberka, CEO, Shell Poland; and Michał Mastalerz, CEO, PwC Poland.

Prof Orłowski set out Poland’s macroeconomic landscape in 2023, stating, “It’s going to be an interesting year with many unknowns. Right now, we are in the middle of the unknowns – politically and economically. The global outlook is mixed. The situation doesn’t look nice, with a possible recession in Germany and the rest of Euroland, and in the US as well. When discussing the ongoing war in Ukraine, it was said that somehow we have adjusted to it. Assuming that everything is like it is today, the war is the main factor making people pessimistic, as is China. Covid gave us a very good lesson about economy and business. At the beginning of the pandemic, Covid looked like a catastrophic event, but we very quickly learnt to adjust. Firms learnt how to operate in the circumstances,” he said. There had been a small Christmas present in the form of indicators published at the end of the year, which showed some slight improvement. “The German PMI was up to 47 from 42, suggesting that recession was inevitable, but it would probably not be sharp and long-lasting. Everything could change – with the madman in Russia – the next three to six months will be tough, but we expect a rebound of the economy,” he said.

“Many unknowns remain. What does it mean for Poland? There are hopes that the second half of the year will be better. Better than 2022? No, because the first half will be difficult. However, in the second half we can hope for an improvement of the situation. There is no reason to be in a panic. Last year’s first half GDP growth looked good but it was an illusion due to unusual behaviour of inventories after the pandemic – 8% growth in Q1, 5% in Q2, 4% in Q3; there’s no data yet for Q4 but it would be close to zero; if so, then we are likely to experience technical recession, defined as two quarters of negative growth. So, we might have -5% or -6% in Q1, but don’t panic – it reflects an unusual Q1 22.”

“Consumer demand has been the main driver of economic growth in Poland in the recent past, which was unfortunate. Government policy has been pushing up demand without creating an environment that drives investment. But despite the controversial policies, foreign investors didn’t panic. Rather, it was Polish SMEs that were put off from investing. This has proved to be a major shortcoming. Poland currently has a 15%-16% investment-to-GDP ratio, which is historically low. The government has been unable to create the right environment. Key point – can you make firms optimistic? It has not been achieved. Consumption is slower and slower, wages not catching up with inflation, investment is unlikely to improve, if you exclude inventories. Exports look astonishingly good, but they must go down, even if the German recession is mild. So the key question is the second half of this year. How impressive will the rebound be? If we have a 3% contraction in the first half, followed by 3% growth in the second half, that would not be a catastrophe, but it’s not a rosy picture,” he said.

“Inflation is a problem,” he said. “Thanks to the fall of global oil prices, there has been an easing of pressure over the past few months. In Germany, inflation has fallen from 10% to 8%. Poland’s fall could have been bigger. Oil price is crucial – even if it is stable, we will still have a hike in inflation over the next two to three months, and then it will decelerate because of base effect.”

Prof Orłowski forecasts inflation peaking at 22%-23% in March, thereafter falling to 15%. He took issue with the president of the National Bank of Poland, Adam Głapiński, who believes that given the current interest rates, we will have single-digit inflation by the end of the year. “Frankly speaking,” said Prof Orłowski, “I’m afraid we’ll be locked in double-digit inflation for a long time. Inflation will stabilise at between 10 and 15% – radical tightening will have to happen to get it back down. It will take a few years before society gives a mandate to the government to do what’s necessary to get it down.”

“Interest rates will stay at the current level, unless there’s an exchange rate crisis.” The government claims that the budget deficit is manageable, said Prof Orłowski. “The situation will deteriorate towards the end of the year, but Poland is not Greece. There is no risk of bankruptcy, but there could be a crisis caused by the central budget deficit being pushed out to other institutions.”

Then there is the question of whether or not Poland will be denied access to EU funding for infrastructure and energy projects because of rule-of-law issues. The money would make the difference between Poland’s public-sector finances “looking pretty good to looking pretty bad,” said Prof Orłowski, with the threat of a downgrade of Poland’s ratings should the funds not come through.

“There are two big unknowns – the first is the madman in the Kremlin. Moods have started to improve in Europe, but this might change if Putin does something in energy. Right now, the temperature in Kyiv is 0C, whilst in Moscow it is -30C. I would be very careful with speculation. Putin has six months to win a war. His most efficient weapon is to cut off Germany’s gas,” said Prof Orłowski. “The second big risk is the Polish parliamentary elections – not so much the result, but what politicians will do to try and raise their popularity. If their response is to increase government spending, and the central bank prints more money, this may lead to a situation with even higher inflation, lasting even longer,” he said.

Adam Uszpolewicz asked each panellist to give their assessment of how they see Poland in 2023 and to comment on what Prof Orłowski had said.

Aneta Jóźwicka said that 2022 was an exceptional year – global events, not only war and the opening of the economy after the pandemic – but also the fact that now climate change is irreversible. “100 million people worldwide have been forced to move; Finland and Sweden are expected to join NATO, there is China emerging from its Covid lockdowns, there are expectations and fears – war, inflation, climate and environmental challenges– people expect that these issues should be fixed by government. What is the expectation from business then? Businesses should address wages, cost of living, manage their costs well to allow lower costs of goods and services, support local communities, and bring manufacturing back home. However, to execute these ambitious goals, business needs a good regulatory environment. We need security and predictability to enable long-term planning and investment. Also, more time should be taken to introduce any new legislation (including a longer vacatio legis). Overall there needs to be a better dialogue between business and regulators; we must showcase our position and strive for a legal environment that is fair, just and predictable,” she said.

“Looking at Poland from the investment perspective, there is a common misunderstanding that the war in Ukraine is the main reason holding investors back. However, if we look at the current investment structure, we can see that some companies have withdrawn from Poland, some have decided not to invest. But that is balanced with investment from the security sector, and those setting up in Poland waiting to rebuild Ukraine once it will be possible. The two main factors affecting investment are unpredictability and supposed instability. Poland needs a better dialogue with stakeholders, whoever wins the election this year. Poland also needs to rise quickly from 40th place to tenth place in terms of ease of doing business around the world.”

“We will be sending a survey to all members of the British Polish Chamber of Commerce asking about their expectations from the chamber; this will help to formulate our strategy and activities for next few years – Poland should be as easy a place to do business as the UK – this is a good target for BPCC,” said Ms Jóźwicka.

Piotr Kuberka outlined Shell’s plans for Poland in 2023, putting them into the general context of the energy sector as it deals with climate change. “This is going to be shaping what happens in the energy market for many years to come. Energy transition means we halve all our emissions by 2030, and get them down to zero by 2050. Decarbonisation will mean continued vertical and horizontal cooperation to win the challenge of climate change. Offshore wind will be an important part of the battle for energy price and energy security. The Baltic Sea has the potential for nearly 100GW of wind power, of which Poland’s share is about 30GW; permits out for 11 GW are being reviewed as we speak. This won’t happen from one day to another, so we will have to act quickly. The war has disrupted supply and demand, Russia’s weaponising of energy has really stretched the energy market, leading to volatile prices in 2022. There will be more changes in 2023. Inflation and its impact on businesses – we don’t know how the war will develop further. The winter has been mild so far this year, so there’s been less energy consumption than expected, but it’s not just this year but the next couple of years. It may become more and more difficult, we need to be thinking about gas stocks for 2023-2024,” said Mr Kuberka.

“All the factors – interventions across the world, governments trying to soften the impact on consumers and businesses are of course helping those in need. However, as we’ve seen in some countries, price caps have disturbed the fuel markets, even leading to shortages. We should all focus on the responsible use of energy, limiting the demand and softening the impact on stretched supply chains and prices. Energy transition, however, remains critical. For this to happen smoothly, long-term predictable legislation that’s friendly for investors, quick permitting from the government, and structures for the future are needed.” Changes in law impact everything and they determine how attractive the market is for BPCC members, he said, echoing Ms Jóźwicka’s sentiments.

Asked by Adam Uszpolewicz whether he should buy a petrol or electric car, Mr Kuberka replied “Buy an electric car! It is the future! Much smoother to drive and more and more charging points appearing on Shell forecourts!” He pointed out that by the end of 2022, there were more than 60,000 electric vehicles in Poland, half of which were hybrid and half full-electric.

Turning to real estate – Savill Poland’s Tomasz Buras said that in general, the market always has to face challenges when interest rates are high. As to prospects for Poland in 2023, he said that there’s a different story across commercial offices, industrial, retail, residential and hotels. In the last three years, between 2020 and 2022, around €17 billion has been invested in Polish real estate. “But with accelerating inflation and high interest rates – we are very cautious for 2023. We should run our household in a very prudent way. As we are not in the eurozone, there’s the danger of inflation. Salaries are growing far behind inflation, especially for young people, so it’s very difficult for new employees to get on to the property ladder; their salaries won’t grow – but the rental market, energy and food costs will go up,” he said.

But turning to commercial real estate, he said: “Perception is sometimes more important than reality! The investment market is very subjective. There are different approaches to risk. One investor might say that Poland is completely off the list, the other will say that we’re the place to invest. South-east Poland has already become the logistics base for Ukraine.

“The cost of money has gone up, and after five years of free money, rents will go up as indexation happens from March; energy costs, tenants renting warehouses, factories, operating costs, renting space will all become more expensive. The strongest sectors of real estate in Poland right now are the living sector and industrial. Residential rents went up; the industrial sector is the second locomotive in Poland; with the increase in the cost of financing, tenants who have production are facing rising costs. Corporate hubs some might invest their own money to buy or develop their own real estate. There is a mortgage crisis. Those who bought apartments and sat on them as a speculative investment, leaving them not fitted out and not lent out will face difficulties, but in the mid- and long term, I can’t see why prices of apartments can come down,” he said.

Concluding, Mr Buras said to his fellow CEOs: “This is the time in which we can prove our worth as leaders and navigators, we must take care of our people, and hope that there will be a more optimistic scenario ahead – until then, it will be a bumpy ride.”

Beata Balas-Noszczyk from Hogan Lovells Poland, set out the prospects for 2023 from the point of view of a corporate lawyer. “A number of the investment bankers we work with see uncertainty and ask, whether there will be an increase or decrease in the volume of M&A transactions over the next six months? This is a time of observation for us. Everybody is nervous, everybody has a plan A, B, or even C. Last year was a boom year for transactions, with profits up 20% worldwide. In Poland M&A transactions were up by 15%; private equity has a great deal of money waiting for the future. My observation is that in terms of transactions, private equity is looking to go shopping, but is waiting for a good price. The trends we have observed are opportunities in nuclear energy, alternative energy, infrastructure, IT, and new technology. In Poland’s financial services market, there is no re-investment, instead, there is consolidation with local players; AXA, Uniqa, investment funds, Nationale-Nederlanden, and pension funds, but locally there is no new investment. The banks are focused on online payments, new technologies, distribution, and fintech. We have a lot of projects, with some very sophisticated solutions close to the market. Covid actually improved the financial sector’s condition by accelerating the digitalisation of banking. Finally, ESG will be a big challenge for everybody. Packaging companies will be asking their clients whether they are ESG compliant. The EU supports ESG projects in order to increase compliance with rules and policies. There will have to be a substantial change in mentality and this will affect all business operations,” she said.

Paweł Bajorek focused on the Polish consumer market in the year ahead, in particular looking at Reckett’s core areas – health and hygienic products – where, he said, “consumers are spending less enthusiastically.”

“2022 was a very difficult year. We faced a big production inflation but increased production costs have not yet been passed onto the market. New, higher prices will be implemented still in Q1 ’23. In food, where margins are thin, price increases were immediate, but in non-food, prices will continue to increase. We could observe in many categories, especially non-discretionary categories, higher volumes as we have a couple of millions of new consumers in Poland in the form of Ukrainian refugees. Higher volumes helped to deliver the year, but in most companies margins are down. Higher volumes and lower margins mean the P&L is unbalanced: the top line is good, the bottom line suffers. How volume and pricing will look this year depends on the situation in Ukraine. We expect 2023 will be equally or even more difficult than 2022. We have had to have very difficult discussions in the business – do we optimise to survive, or do we take losses and invest to win in 2023 and beyond? Prof Orłowski expects the first half of this year to be bad, the second half to be better. We see it the other way round; in the first half we still expect higher sales than during H1 2022, mainly due to the higher consumer base. In the second half it may get worse as the base is already high. This impact would be strengthened if millions of Ukrainians leave Poland to go home, leaving us with much lower consumption and much higher prices. So investment decisions regarding Q3 and Q4 need to be taken.”

He continued: “There is a big shift in channels going on. The position of discounters will strengthen. In e-commerce, the pace of growth – boosted by the pandemic – will stabilise. There is a huge battle between private-label and branded goods, and between brands themselves – a fierce battle to protect market share. So 2023 will be a balancing act. Do we push more to protect margin, taking a hit on volumes? This will affect our production lines – set up on the expectations of booming volumes – or do we take a hit on margins and therefore the bottom line, to protect our investment decisions in our factories, in anticipation of a coming upturn? So, while H1 should still be OK, H2 will be a real challenge, and then we’ll see who will have taken the right decision,” said Mr Bajorek. He was more optimistic on the long-term inflation prospects for Poland: “we expect it to get down to 4%-5% after 2023, rather than the 10%+ mentioned by Prof Orłowski.”

Michał Mastalerz, the new head of PwC Poland, began by pointing out that Poland now has 400,000 people employed in the business-services sector. He set out the challenges as he sees them facing the entire business ecosystem in Poland. “We work with energy, real estate, FMCG and other sectors, and while we try to be more optimistic, the CEOs of private businesses in Poland are telling us that recession is coming, and we’re cutting marketing expenses. ‘You are next’,” he laughs. But this is not the time to stop addressing the challenges that are still facing business, said Mr Mastalerz. “These include reviewing current business models; implementing new IT systems – in particular, transition to cloud and cybersecurity. Governments are ready to take energy transformation seriously – businesses need to do so too. Cost control is particularly important in troubled times; energy costs and finance costs are hurting businesses. For us, the internal challenge we face is the pressure on salaries. We must take care of our people, invest in our people. But with current concerns about inflation, geopolitical turmoil and the economic downturn, isn’t looking after our employees an even more pressing issue than ever before?

“Macroeconomists indicate that the coming slowdown will not necessarily translate into a significant increase in unemployment. This news may please employees, and should also prompt employers to act to invest in employees and build a welcoming workplace for all. Just as paying taxes is a constant part of life, competition for talent is and will continue to be inevitable,” he said.

In the Q&A session, Prof Orłowski was asked about the influence of the Russian invasion of Ukraine on the Polish economy. He replied that the three million or so Ukrainian citizens that have passed through Poland were quite the opposite of the typical stereotype of refugees, who arrive without money, and are a fiscal cost not a benefit to the host nation. “In particular, in the labour market, with millions of people suddenly coming into the country, one could have expected to see an immediate increase in the unemployment rate – but no. Young Ukrainian men have left Poland to defend their country. So overall, we have not been seeing a fundamental impact on Poland. The question rather is long-term – how long will they stay? At least a part of them will stay on even after war is over; it’s not our choice. Rebuilding Ukraine, the West will pay, tens of billions of euro will be spent on that. It’s not Iraq. Poland has a strong position, and the general perception of our country has been very positive, on the front line to help Ukraine. So the balance is positive for Poland. In the short run, it’s a surprise for Poland, nobody knows why, it depends on how long the war will last.”

There was another question about the high-end Ukrainian refugees, who could afford private schools for their children. In the up-market areas, wealthy Ukrainians have created mini-booms here and there across the Polish economy, but are the wealthy in general recession-proof? High-end consumers are generally immune to crises, said Reckitt’s Paweł Bajorek, assessing that “people who do well will be OK for next two-three years, they will make cuts, but are unlikely to economise on their children’s education. Sales of premium brands are still growing, says Aneta Jóźwicka, but the number of cost-conscious consumers is also increasing, “According to Kantar Global Barometer, 71% are aware of prices, and 29% will buy whatever is on promotion,” she said.

An interesting point appeared in a discussion about the banking sector – since the financial crisis, banks have been drawn into public ownership, and have therefore been more connected with public policy, and less independent. “Post-2008, said Adam Uszpolewicz, “with the rescue of banks by governments, the concept of banking as we had hitherto understood it ceased. Banks are not allowed to take big risks, because taxpayers’ money is used to bail them out when they are in trouble. Thus, banks are seen as utilities and are not allowed to make big profits. In the old days, a return on equity of 25% was common, now it’s nearer 8%, 4%, 2% even. In Poland, with this government’s repolonisation programme, almost half of the sector is in state hands. Beata Balas-Noszczyk added that governments should be supporting banks otherwise entire economies might collapse. Michał Mastelarz observed that it is easy to target banks and bankers, but that they are no longer such an easy target, because the financial performance of banks is under very high pressure.

Answering a question about the EUs’ Green Deal, Fit for 55, Re-power EU, circular economy and non-financial reporting programmes, Piotr Kuberka from Shell said that green transition will be a long-term project. “Big changes need focus, delivery time, permits, legislation, funding, investment and the right grids. Nuclear power requires a long-term approach, massive changes are needed, then there is solar energy, the onshore wind problem (10H height regulations). These are the changes and accelerations that the government can make, and investors are looking for. Poland may be behind in some aspects of energy transition but this means that investors can see opportunities, feeding into higher economic growth from the energy transition journey – building turbines or other elements for transition. More and more companies are asking questions – how green is your product or service? Across supply chains – we expect more and more for the participants to be green,” he said.

Aneta Jóźwicka, speaking on behalf of a global company listed on the stock exchange, said: “for investors, if we speak about ESG or profit, results generated by companies are still ultimately the most important; profit makes all the difference,” she said. “However, you have to generate money to invest in ESG. Although investors put emphasis on results they are also very much aware of the requirements of societies, therefore ESG importance grows substantially!” When Polish consumers list their main concerns, she said, the responses are “90% war, 50% economy, and only 33% climate.” But the number of respondents citing climate as a concern is growing, and it will grow further if they experience extreme summer heatwaves, an unusually warm winter or when some climate situation impacts their daily lives. “Consumers are expecting us – business – to take the lead,” she said. Michał Mastalerz said that on ESG, “some clients are really aware, others are still not. But the important questions facing all companies, and this will come to Poland, is the cost of loans based on how firms focus on their progress on transition. Our more educated clients ask us about our ESG policy – we take our non-financial reporting very seriously ourselves. In addition, we are also very strongly strengthening our support team for clients regarding ESG regulation.” Tomasz Buras said that with real estate contributing up to 40% of emissions, ESG had become the number one topic for conferences last year, in particular end-of-life of buildings, new buildings on old sites, managing your buildings, and improving them so they are ESG-compliant. He stressed the previous speaker’s point: “greener buildings will get cheaper money – based on the EU taxonomy”.

Summing up, Prof Orłowski said that we are at a turning point in history. Beginning with the financial crisis of 2008/9, the pandemic, the global logistics crisis, a security crisis, an energy crisis – “this is not a collapse, nor is it the end of these crises – there are still some shocks due in the future. The environment – there has not yet been a shock that has changed people’s views – but it will happen and it will change the direction of globalisation, and businesses will have to adjust to it. As it becomes a reality, after five years, we will see that we have been living through a big, big, big, change.”